Guaranteed annuity income sounds nice

Annuities can seem attractive to many retirees. It is a regular paycheck into your account. It’s an easy way to turn your lump sum savings into a regular fortnightly income.

One of the main annuity providers in New Zealand is Lifetime Income. You invest your money with them and you are guaranteed a certain amount of income every fortnight for the rest of your life. Even if your investments lose money, Lifetime income will still pay you the same flat amount every fortnight. If your investment balance grows, so does your fortnightly income.

Sounds amazing right? No downside risk of losing money due to low interest rates or investment losses.

I punched in some numbers on their calculator using the assumption of a 65 year old single person with a PIE tax rate of 17.5%, wanting to invest $300,000. Under this scenario, I would be guaranteed at least $415.38 per fortnight ($10,800 per year) for life. If my investments increase beyond $300K then I will receive 3.6% for every extra dollar.

A return of 3.6% after taxes and fees. Not too shabby I must say.

The older you start, the higher your return. Using the same assumptions but for a 75 year old, Lifetime Income currently guarantees returns of 4.6% per year.

They invest the money in a balanced fund so some years returns will be greater than 3.6%, whereas other years returns will be less than 3.6%. In the years where your investments return less than your guaranteed income, Lifetime will draw down from the capital in your fund reducing your investment balance. This will not reduce your regular payments. It will reduce the likelihood of your investment balance growing though.

Why annuities are not as attractive as they seem

All this sounds great, so what is the downside?

Inflation.

Your fixed income of 3.6% is not inflation adjusted. So how does this look in reality.

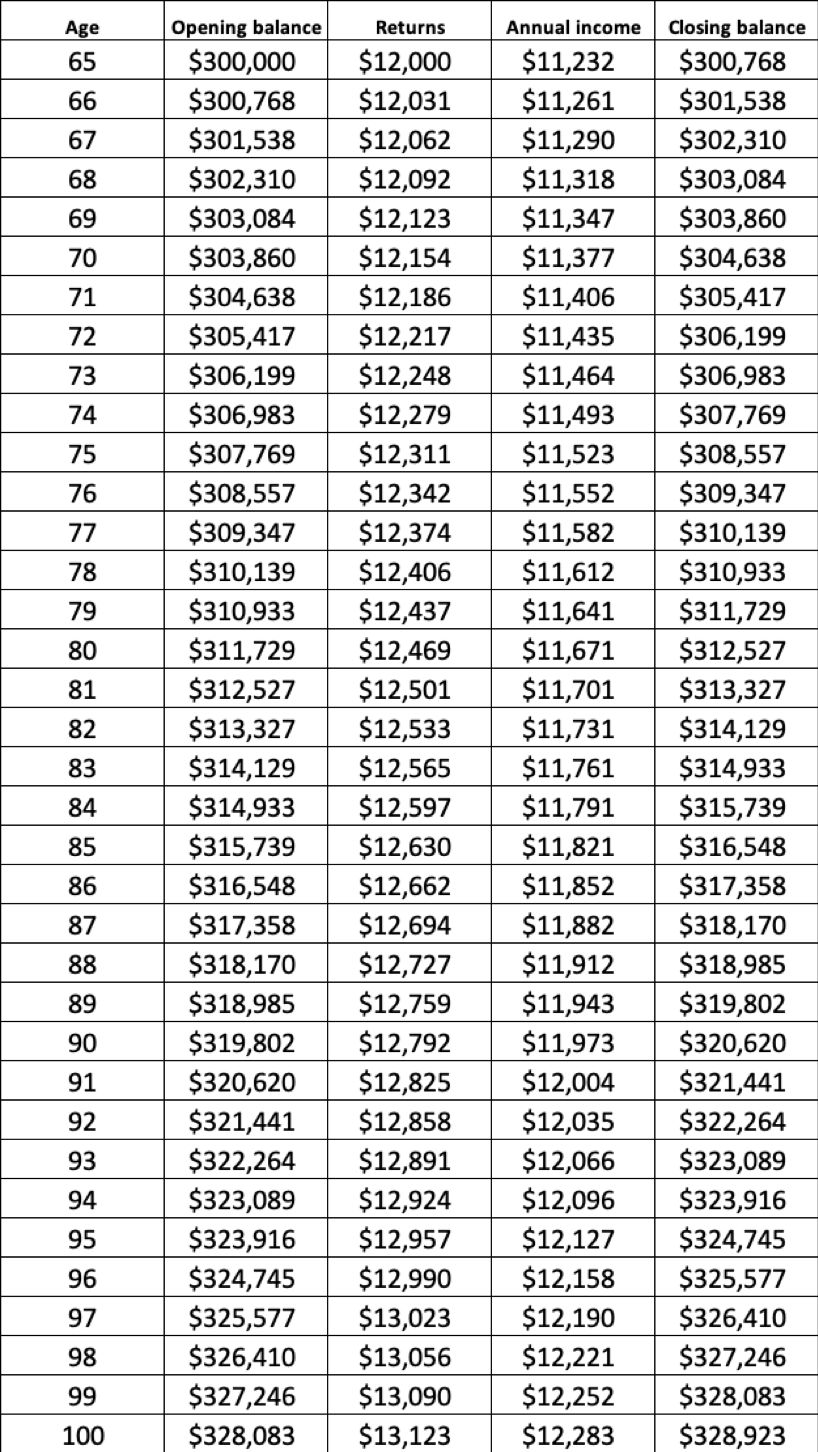

We will again assume you initially invest $300,000 at age 65 with a guaranteed 3.6% income. We will assume the fund returns 4% per year (after fees and taxes), so your balance does grow each year. We will assume inflation is 3%. So how will your regular payments look in the future?

Annual annuity payments

At age 100, your annual income will have increased to $12,283. Great. Don’t get carried away. We haven’t bought in inflation yet. How does it look now once we include the decrease in purchasing power?

We will assume your annual expenses are $40,000 and increase each year with inflation.

The impact of inflation on fixed annuity products

Your first year of annuity income will be $11,232, which is 28.1% of your annual expenses covered.

By age 100, your annuity income will only cover 10.9% of your annual expenses.

This means with each passing year your annuity income will provide for less and less of your retirement lifestyle and you will need to find the extra income from elsewhere. Or in other words, at age 100 your annual income is only $3,750 in today’s dollars. Much less than the $11,232 you will originally be receiving.

Of course inflation could be more or less than our given assumptions. If more than 3% then the results will be even worse. If less than 3% then it would look slightly better. You can also combat inflation by spending less as you age, but this is not always possible.

I have written more about annuities in my retirement series here.

Annuities can be an option for some people, especially if it is only a portion of your retirement pie. They do become more attractive the longer you can delay starting out. But if you are looking at being in an annuity for over 20 years, then just be aware of the impact of inflation. It is a silent but lethal beast and you may find in your later years that your annuity is not providing enough.

If you need help with your personal retirement planning, then get in touch today.

The information contained on this site is the opinion of the individual author(s) based on their personal opinions, observation, research, and years of experience. The information offered by this website is general education only and is not meant to be taken as individualised financial advice, legal advice, tax advice, or any other kind of advice. You can read more of my disclaimer here