In the last couple of years, I have provided annual updates on the affordability of NZ housing, and thought I would continue that trend in 2026. You can read previous summaries here and here.

Over the last year, we are experiencing interesting times where unemployment is creeping up, but house prices and mortgage rates have been trending down. I suspect that houses are more affordable than they were a year ago, and much more affordable than two years ago, but lets dig into the data.

Are monthly mortgage payments affordable?

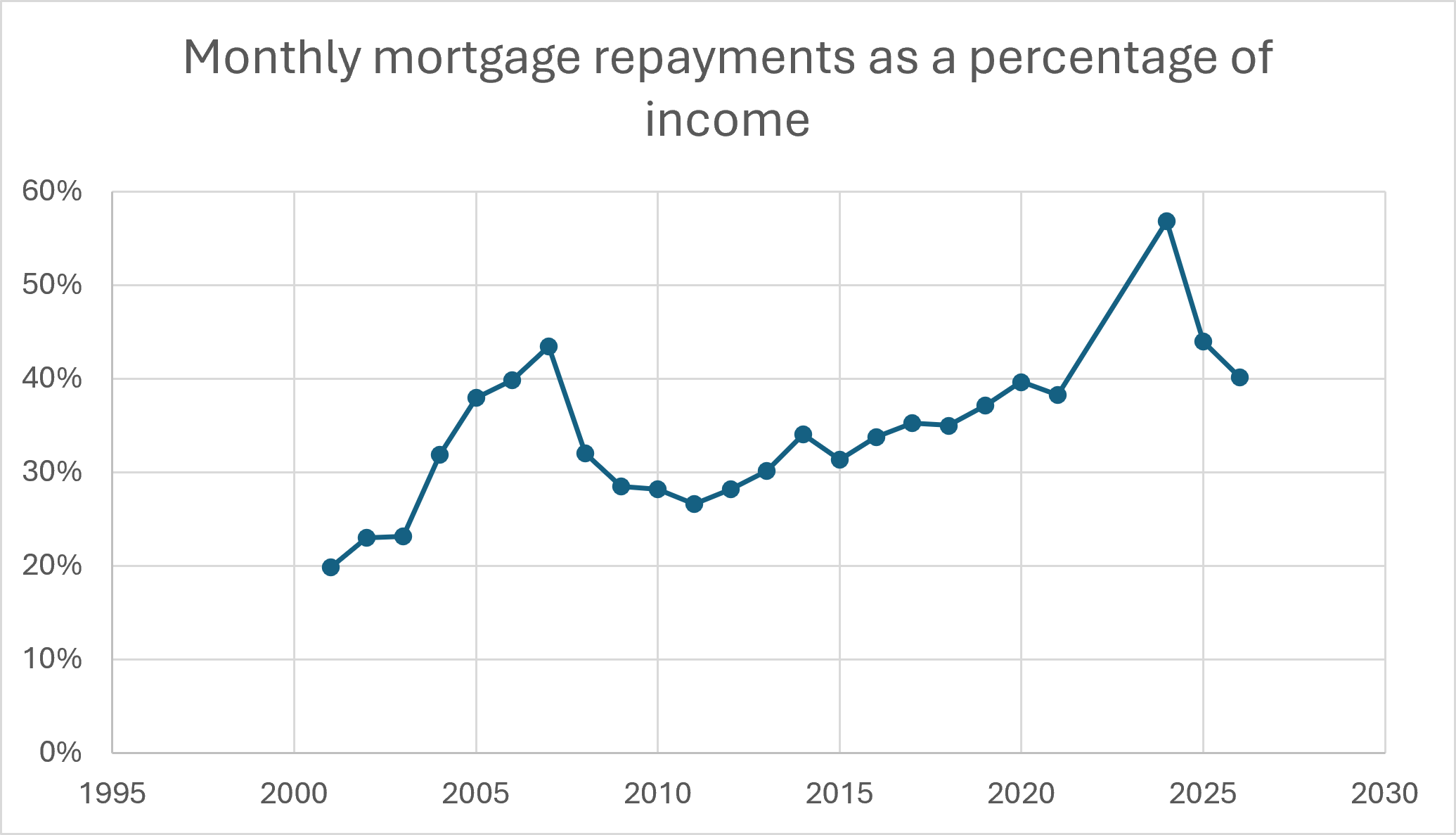

Monthly mortgage repayments as a percentage of income

Affordability is best measured by using monthly mortgage payments as a percentage of gross income.

This particular data assumes a 20% deposit on a 30 year mortgage.

The current data is:

Floating interest rate of 6.2%. A drop of 0.6 percentage points from one year ago

Median nationwide house price of $770,000. More or less the same as a year ago.

Median household income of $112,840. 2026 median household income data has not been released until June 2027, so this assumes a 3% increase on 2025 which should be close to projections.

So with a 9% drop in mortgage rates, 0% drop in house prices, and 3% increase in income we see the median monthly mortgage payments drop from $4,016 a month to $3,773 a month, which is a drop of $243 a month from 2025. A drop from 44% of median household income to 40% of income.

The picture for buying a home looking much better than it was one year ago.

A mortgage of 40% of income is still high by historical standards but about on par with 2020-2021. This is also pre tax income too, so the percentage of in the hand income is much higher. Also don’t forget you still need to pay for other home ownership expenses such as rates, insurances, maintenance, and so on. Housing spend still taking up over 50% of after tax income for many people. But at least there has been a little relief in the last year. Also, many home owners are on lower interest rates than floating rates so that will help bring the per cent of income number down a little too.

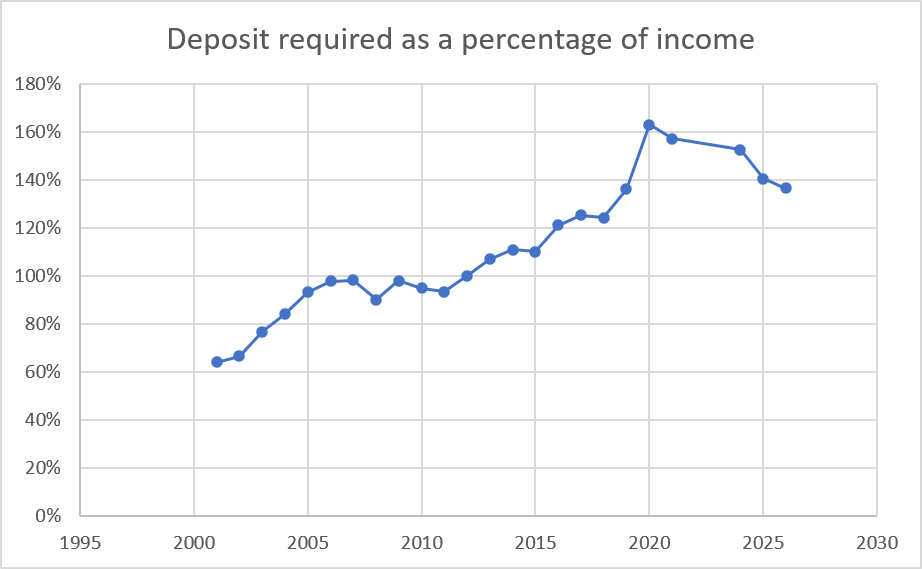

Owning a home is one factor, but how about actually buying a house? Is the situation better for how long it takes to save for a deposit?

How long does it take to save for a house deposit?

House deposit required as a percentage of income

The amount of pre tax income it takes to pay for a medium priced home ($770,000), with a 20% deposit ($154,000), on a medium household income ($118,660) has dropped from 141% to 136% in the last year.

The time it takes to save for a 20% deposit still more or less around 10 years. House prices remaining static with a small increase in income hasn’t moved the needle much.

Final thoughts

The nationwide data is showing a slight improvement in affordability compared to a year ago for the average kiwi. But with job security and unemployment still uncertain, as well as signs of inflation and interest rate increases, people are by no means rushing to buy houses. And as always, there are regional differences that you can see in my housing affordability calculators.

It will be interesting to revisit things in a year to see where affordability stands. A lot will depend on the state of the employment market and the speed and magnitude of inflation increases. Although it is better buying now than one year ago, it is still not very affordable by historical measures. But if your employment is secure and you plan to live in the home for many years and can afford to buy, now is always going to be a good time.

I have added a couple of housing affordability calculators and resources that you can view historical affordability statistics, as well as your own personal affordability levels. You can find them here.

If you need help with any financial decisions , then get in touch today.

The information contained on this site is the opinion of the individual author(s) based on their personal opinions, observation, research, and years of experience. The information offered by this website is general education only and is not meant to be taken as individualised financial advice, legal advice, tax advice, or any other kind of advice. You can read more of my disclaimer here