I have many clients approaching retirement that have a lot of their money, if not all, in one fund. Such as a growth fund, balanced fund or conservative fund.

When building your investments this isn’t the worst thing. In fact, many funds are diversified enough that it is all you need. Although, I prefer a more individualised investment approach, the simplicity of it isn’t a bad thing at all.

The problem lies when it comes to your retirement or when you need to start withdrawing from the fund.

You don’t get to choose to withdraw from bonds or stocks. You have to withdraw from the fund as a whole. So if stocks are having a terrible year and are down by 20%, you don’t get to decide to sell the bond portion of the fund. You have to sell some stocks, cashing in your losses. How much of a loss depends on what type of fund you are in.

Whereas the beauty of having separate stock and bond funds is that you decide which to withdraw from depending on how well or poorly the markets are doing. So when stocks are doing well, that would be a good time to sell some stocks, and when bonds are doing better, you can sell down some bonds. That flexibility is what will give your money a far better chance of lasting longer, than the one fund portfolio.

investing in retirement (decumulation) in not as simple as when working (accumulation)

Although separate asset classes are more difficult to manage, it doesn’t have to be that hard. If it is all too much, an independent financial adviser should be able to help with your withdrawal strategy.

I’ll just show the impact of this flexibility with a couple of graphs.

I have assumed a random mix of returns for a balanced fund and one stock fund/one bond fund portfolio. I will assume you start with $750,000 and you need to withdraw $35,000, plus inflation, a year. Average returns of 6% after fees and tax. Inflation of 2.5%.

Over 30 years the two different portfolios will look like this:

Results of withdrawals in retirement from a balanced investment fund

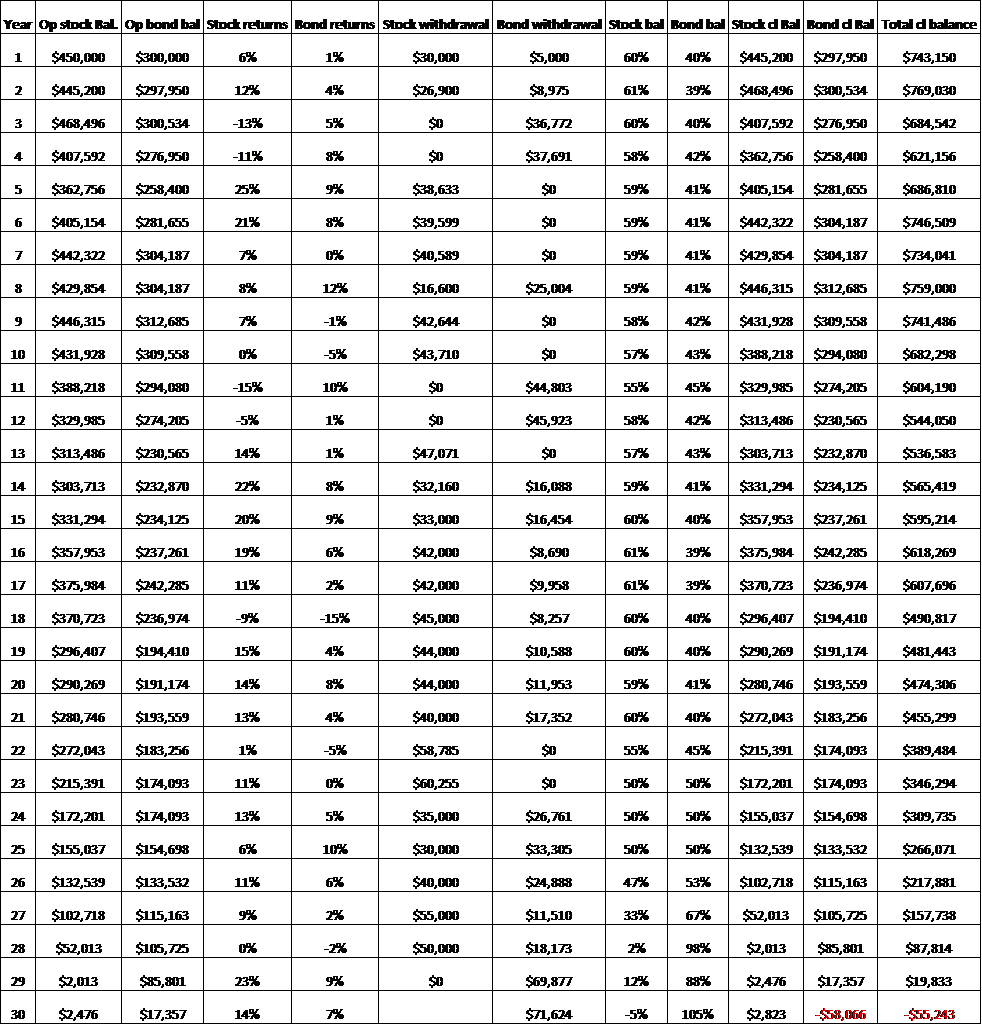

Results of withdrawals in retirement from a 60% stock and 40% bond investment portfolio

This second table is very small, might help if I show visually on a line graph.

Results of retirement withdrawals between a stock/bond portfolio vs a balanced portfolio

The balanced fund running out of money in the 27th year.

The stock and bond portfolio running out in the 30th year.

An extra 3 years of spending ($165,000) by managing separate funds and rebalancing.

Same expenses, same investment returns, same opening balance. The only difference is how you use it.

That could be the difference between having enough money or not, so it’s a very important aspect of retirement planning.

If your returns are higher, investment balance is higher, or expenses are higher, then the difference between the two portfolios will be even more.

Simplicity of investing works very well on the way in, not so well on the way out. Your retirement needs a bit more attention than when you were contributing to your accounts. A more aware investor can do more with their money, making it stretch further.

This is a downside to investing in an all-encompassing fund that I rarely see mentioned.

An extra $165,000 of spending money, in this scenario, is a great return on your time and attention. Even if you have to pay a financial adviser a few hundred dollars a year to manage this for you, then still well worth the investment.

If you need help with your personal retirement planning, then get in touch today.

The information contained on this site is the opinion of the individual author(s) based on their personal opinions, observation, research, and years of experience. The information offered by this website is general education only and is not meant to be taken as individualised financial advice, legal advice, tax advice, or any other kind of advice. You can read more of my disclaimer here