Retirement and the difference of 1% returns

When many of us retire we are well into our 60’s and tend to be pretty conservative with our investments. And fair enough. We have hopefully built up a significant stash by now, and any large losses could be quite devastating.

Just before we finish work is generally the time of our lives where we have the most money we ever have. So a 30% loss on $500,000 when we no longer have income coming in, has a much more significant impact on us than a 30% loss on $300,000 at age 50 while we are still working.

We have more time to recover and we have the income coming in so we have the ability to recover. Not so, once retired.

So I understand the need to be conservative with your investments. But are we being too conservative?

Are we being too conservative with our investments?

If we assume:

A starting balance of $700,000 invested assets

Expenses of $50,000 adjusted for inflation

Pension income of $16,000 adjusted for inflation (single person)

Invested 60% in growth assets such as stocks, 40% in conservative assets such as cash and bonds.

After fee investment returns of 5%

Inflation of 3%

A timeframe of 35 years

We get the following chart:

Investment balance with 5% investment returns

Running out of money after 25 years.

What if we increase the return assumptions from 5% to 6%?

Investment balance with 6% investment returns

We don’t run out of money for 30 years. An extra 5 years’ worth of spending from a 1% increase in return here.

Much better.

However, the real benefit can be seen where we don’t run out of money, but are close.

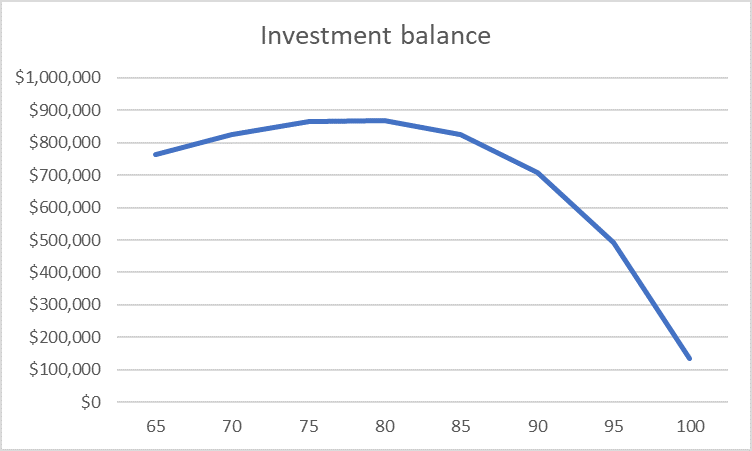

We will keep all the same assumptions as the original example, except we will spend $40,000 per year, instead of $50,000.

Investment balance saving $10,000 a year more

We will squeak home with $133,000.

Increase the returns from 5% to 6%:

Investment balance saving $10,000 a year more and 6% investment returns

Over $1 million left at age 100. A huge difference from just 1% extra in returns.

That provides much more of a margin of safety.

I am not encouraging you all to go out and buy stocks. Or heaven forbid Bitcoin. Especially if you need the money in less than 10 years. That’s the last thing I am saying. These are only manipulated numbers to show a point of how important it is to make sure that you strike a balance between your risk tolerance and maximising returns.

Otherwise inflation may eat your money. It’s not enough for your portfolio as a whole to match inflation. You need to beat inflation or you will be going backwards. And if you are going backwards you will need to ensure you have enough of a nest egg.

This is a very simplified example. It doesn’t include the value of your house and how that can be tapped into, etc. Returns never happen in a straight line, and neither do spending or inflation.

The point is investing conservatively may seem, well, conservative. Safe. But the real risk of playing it safe is returns not keeping up with inflation. In reality then, over the long term, investing too conservatively is a huge risk in itself. Possibly more so than investing more aggressively. Find your balance.

Keeping an eye on investment fees you are paying to fund managers are important too, as it is returns after fees you should be worried about, not returns before fees. Make sure you are comparing apples with apples.

If you are unsure on an appropriate portfolio allocation or how to plan for your retirement, always seek advice from an independent professional. A good one will save you a lot of money and stress.

The information contained on this site is the opinion of the individual author(s) based on their personal opinions, observation, research, and years of experience. The information offered by this website is general education only and is not meant to be taken as individualised financial advice, legal advice, tax advice, or any other kind of advice. You can read more of my disclaimer here