There has been a lot of talk about the rise of artificial intelligence and how it may render Financial Advisers redundant. I am already hearing about people turning to AI for financial advice.

So I decided to purchase Claude Pro by Anthropic to explore the advantages and disadvantages of artificial intelligence head on.

One of my first “conversations” was to explore how good a Financial Adviser Claude is.

With that in mind, I asked Claude to provide an investment plan for a hypothetical situation. I used two different prompts. The first one was with very limited information from the perspective of someone that doesn’t know a lot about investment planning or personal finance. The second prompt was from someone that is well in control of their finances and knows just what information is required.

SITUATION ONE: Financial advice from Claude AI for someone who doesn’t know anything and relies on AI|

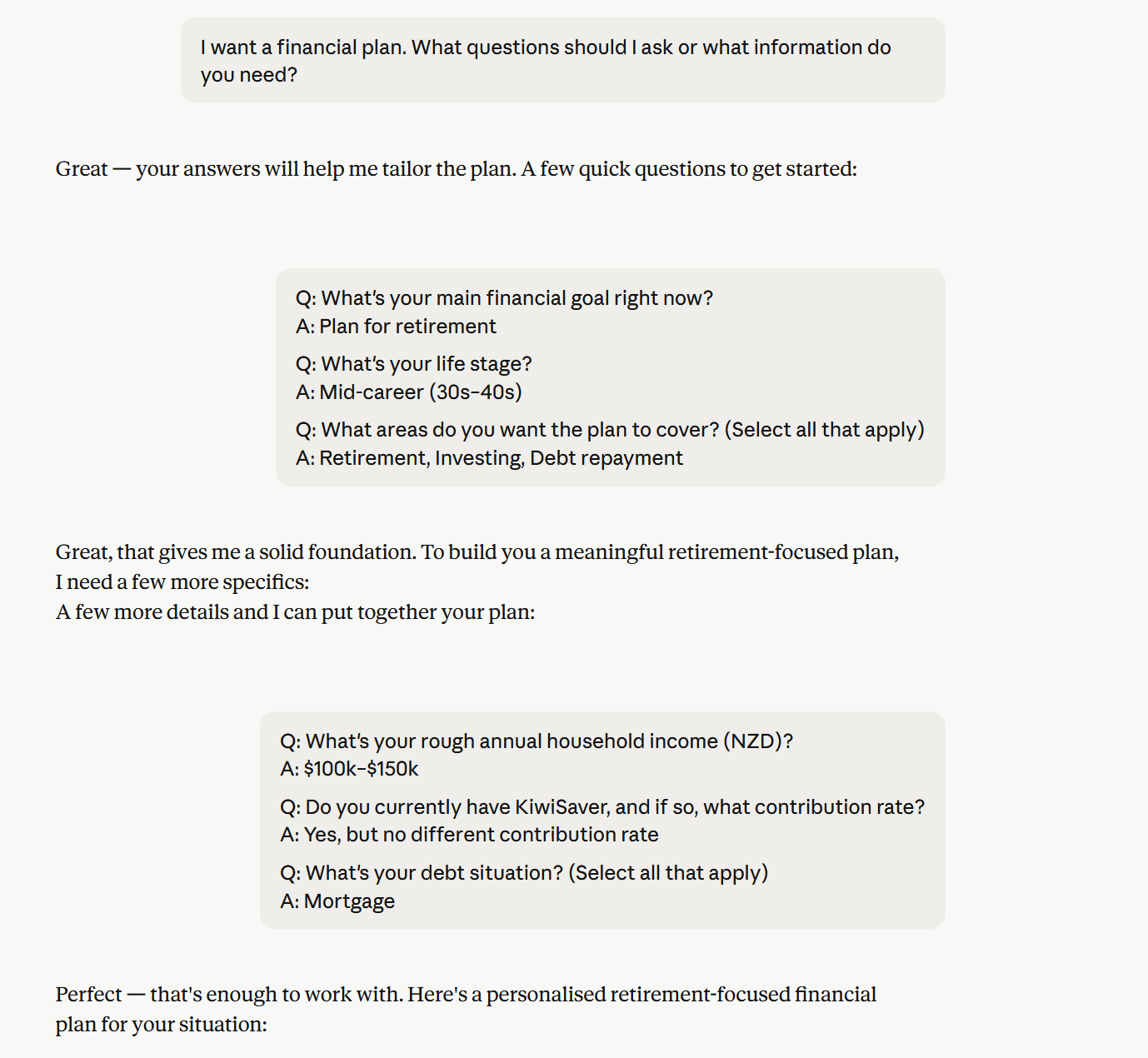

As a novice financial planner in this example, I didn’t know what information to provide so prompted Claude as follows:

Quite a comprehensive response from Claude. A few notes on where I think the advice could have been better:

Kiwisaver

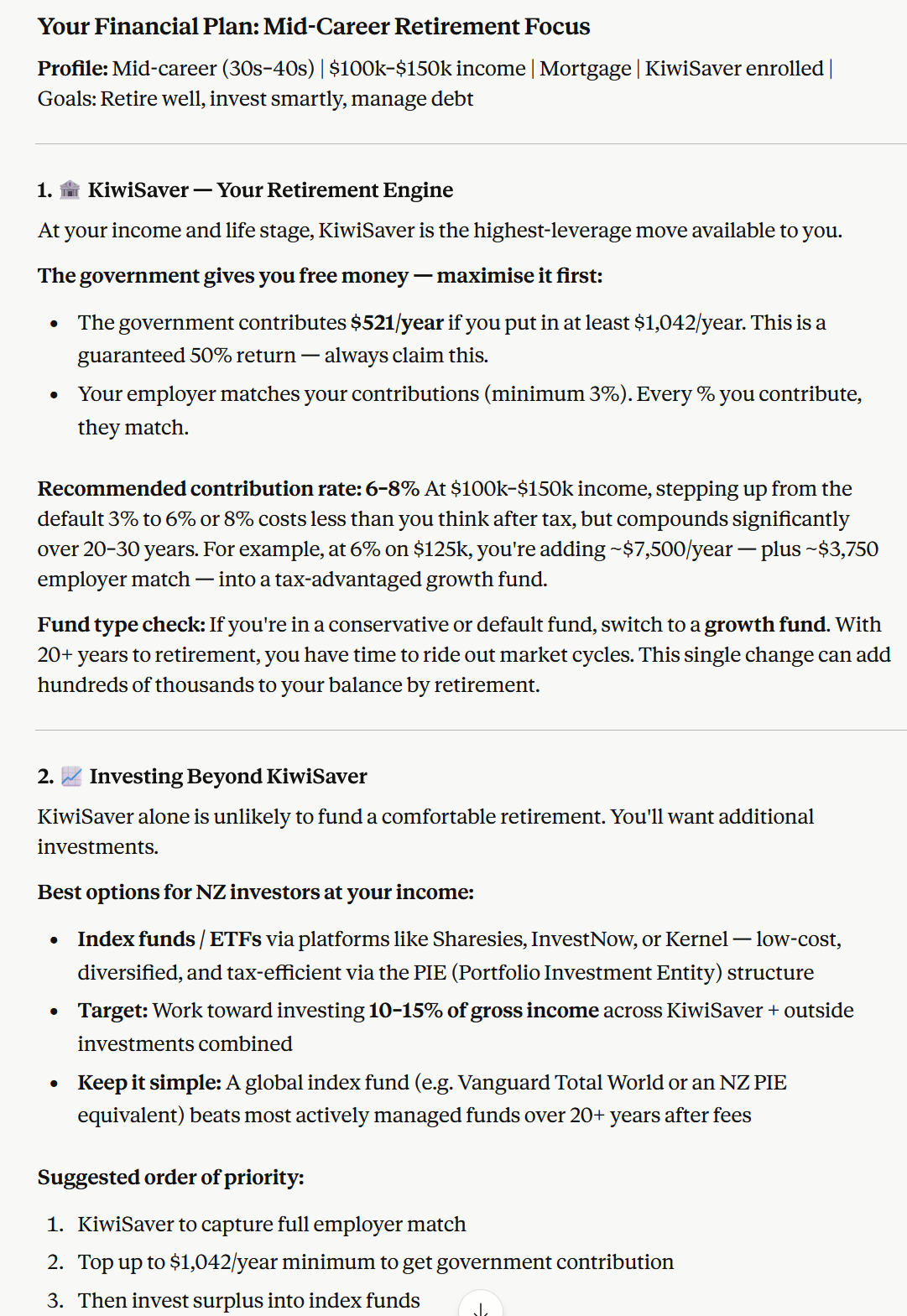

Claude states that the government will contribute $521 a year towards my KiwiSaver. But since July 2025 (almost a year ago), the government only contributes half of that. Claude AI is way behind the times and overselling the benefit of KiwiSaver.

Claude states categorically that my employer will match my contributions towards KiwiSaver. But there are a lot of self employed people out there that don’t get that benefit. Claude didn’t even ask for this distinction. Likewise, for employees on a total remuneration contract, there is no added benefit to having the employer contribute towards KiwiSaver, because if they didn’t their contribution would just be paid as part of salary instead.

Claude recommends increasing KiwiSaver contributions to 6-8%, but why? They mention compound growth but I would have thought it would be better to invest that extra money outside of KiwiSaver. That still achieves compound growth, but without the withdrawal and fund option restrictions of KiwiSaver.

Claude recommends a growth KiwiSaver fund. I provided Claude with an age bracket of 30-40. Growth funds are typically around 80% allocated towards growth assets and 20% towards conservative assets. With over 20 years before access to KiwiSaver, I would suggest an aggressive fund be a better option than growth for most people. This could be the difference of many thousands of dollars for some.

Investing

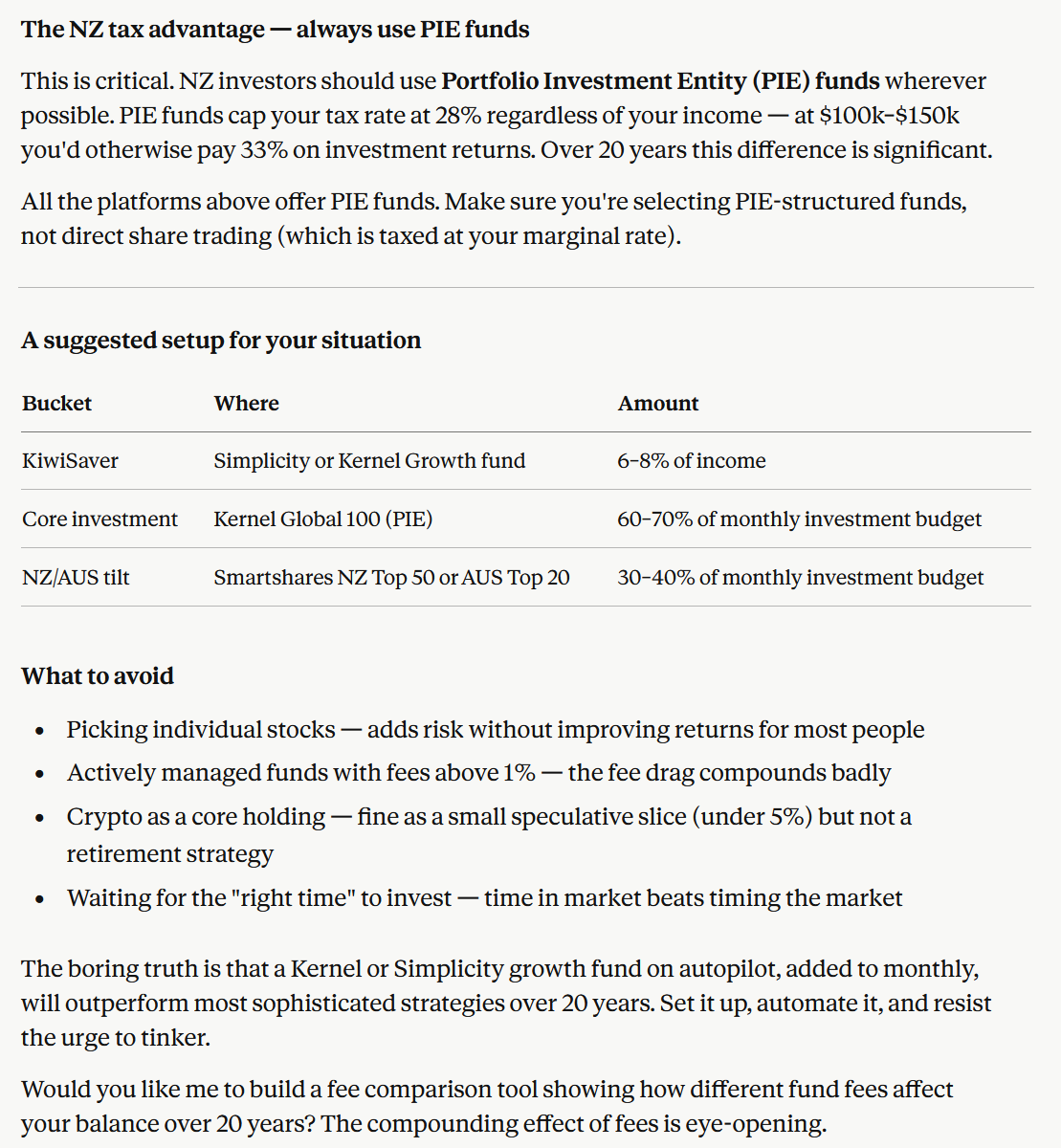

It’s good that Claude suggests low cost investment funds. The data supports this recommendation and I tend to recommend low cost index funds myself. However, there are no specifics provided. Which world fund? Which NZ fund? What percentage into each fund?

Claude also suggests saving 10-15% of gross income (including KiwiSaver), yet Claude had no information on how much I am spending per year nor how much I may spend in retirement. Without that information, they may be recommending an amount that is far too little or far too much.

Mortgage

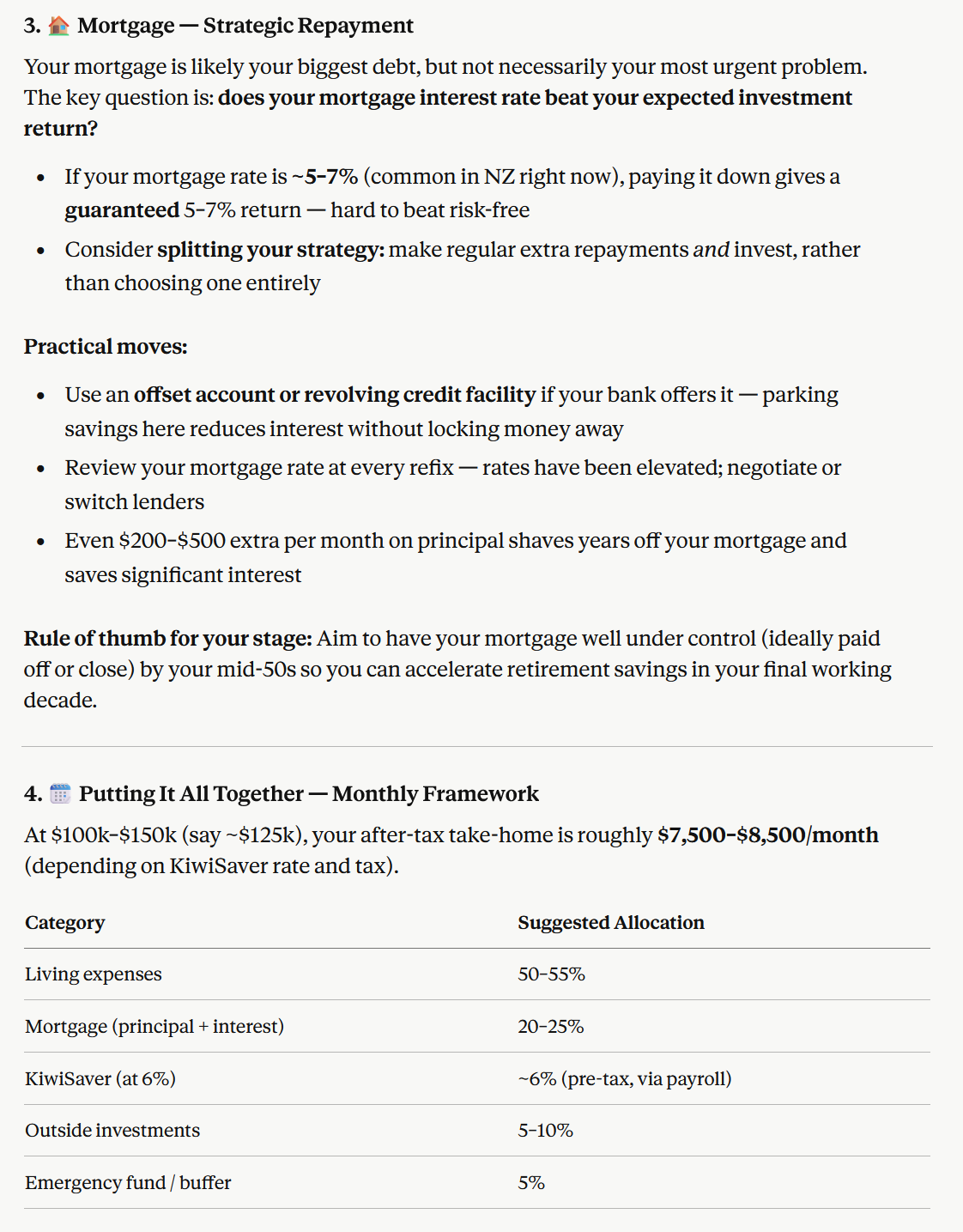

Claude recommends splitting up the mortgage and fixing some and putting the rest on on revolving credit or offset. But again there are no specifics. How much on fixed? How much on offset? It’s general information but not very actionable.

Claude suggests a mix of paying down the mortgage and investing which is good. A lot of people think of this decision as one or the other. Pay down the mortgage or invest. Yet the answer typically lies somewhere in the middle, which AI has got points for this. However, the specifics are again lacking. How much towards the mortgage and how much towards investing?

General info

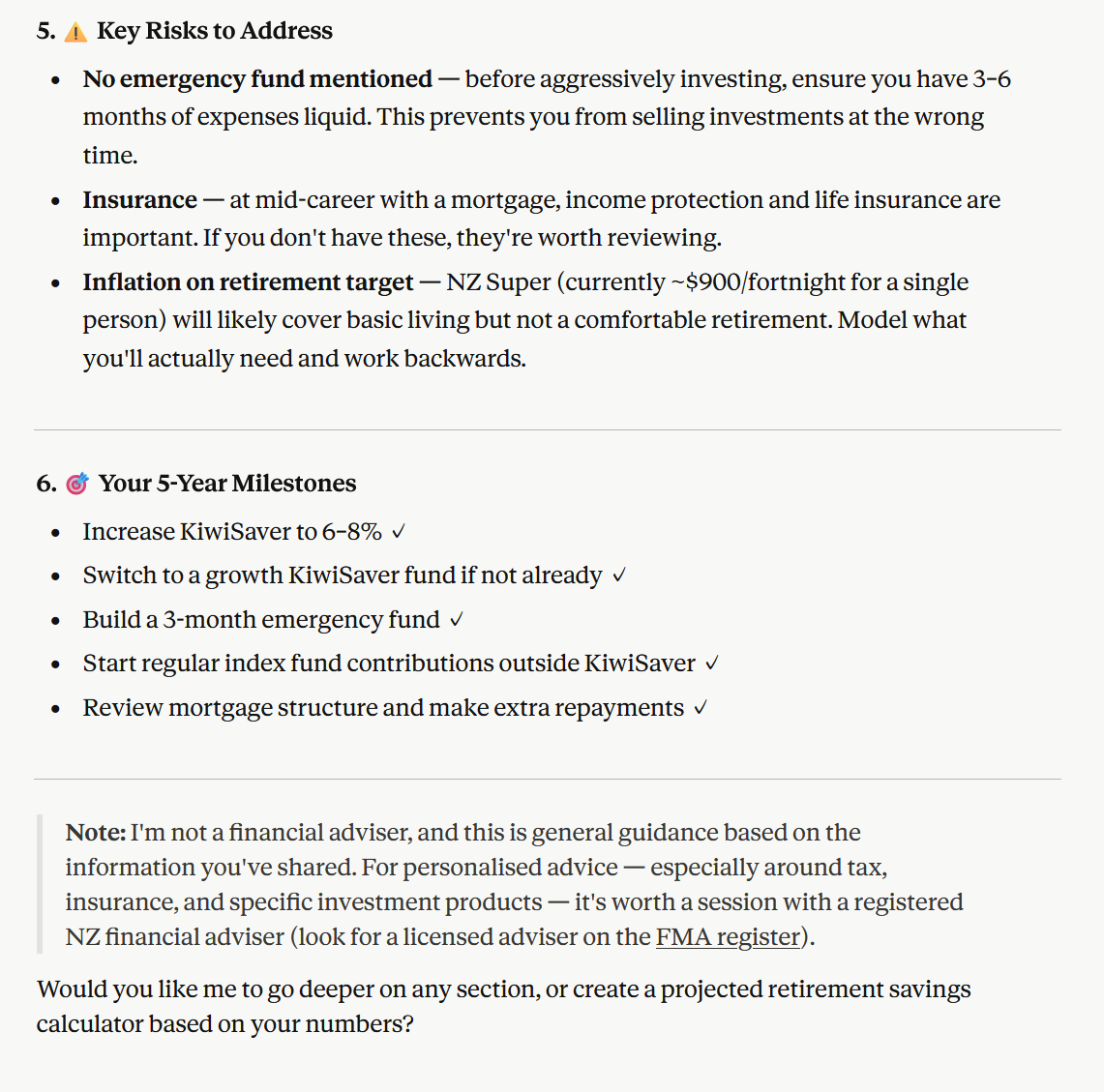

Claude suggests I look into getting life insurance but they don’t have much understanding of my situation. I didn’t provide Claude with information on my family life. I could be single with no dependents. What good would life insurance be there?

Claude also suggested mortgage and income protection insurance, but again had no idea about my situation. I provided no information about how much mortgage I had left or what my current assets were or if I were about to receive any significant sources of wealth through an inheritance. If the mortgage is low or if I had a lot of savings outside of KiwiSaver, then mortgage and income protection may not be that useful for me. Just adding unnecessary costs.

Claude didn’t ask what assets I currently held or what my savings rate or annual spend was. Big omissions that make it very hard to provide reasonable advice. A good adviser will ask questions of you when there is information missing.

3 months emergency advice is a common rule of thumb. It works for some people in some situations, however it is definitely not the right advice for everyone.

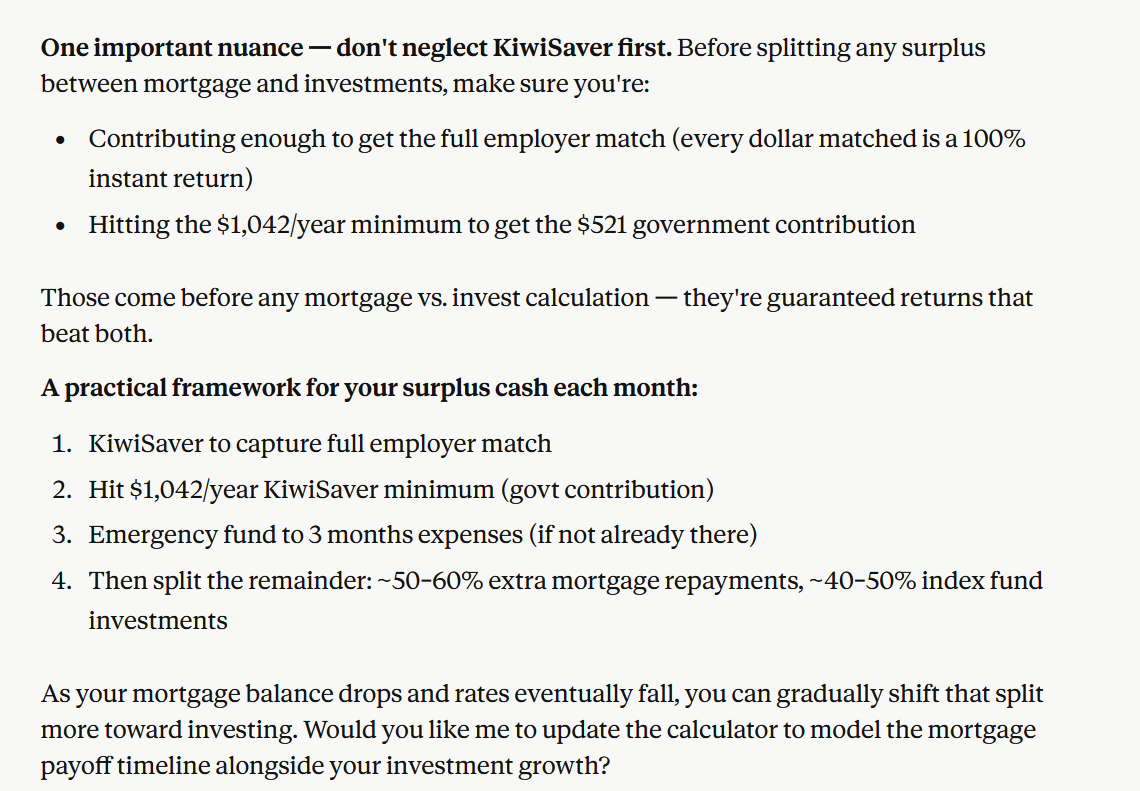

I also asked where I should keep my emergency fund and Claude responded with online savings accounts at a bank or a term deposit. Well, term deposit is terrible advice for an emergency fund. It is not as accessible as other options. Secondly, for most people with a mortgage, a better option than savings accounts is putting it towards the mortgage, either in an offset or revolving credit account.

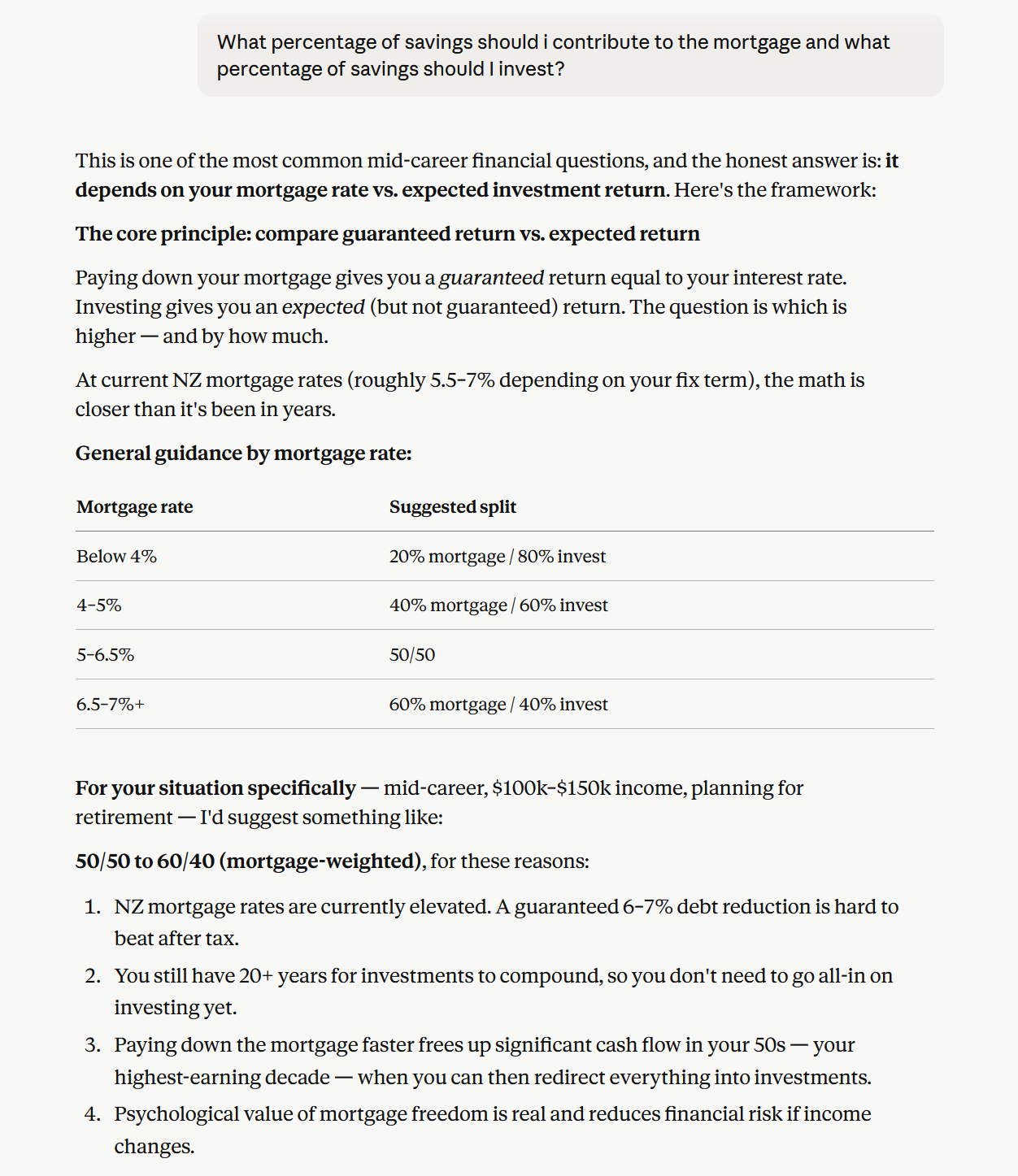

Next I asked Claude how much I should put towards the mortgage and how much I should put towards investing to try and get some more detail or actionable steps. The age old question. Here is Claude’s response:

Claude suggested a mix based on current mortgage rates. At 5% mortgage rates it suggests a 50/50 mix. I don’t mind the advice as many see it as either or (invest or pay down mortgage). I like that the answer is both depending on mortgage rates. But that’s where the positive feedback ends. AI didn’t allow for short to medium term spend. If I need money in the next 0-9 years then paying down the mortgage or investing in shares is not the best. In fact, it is downright bad advice.

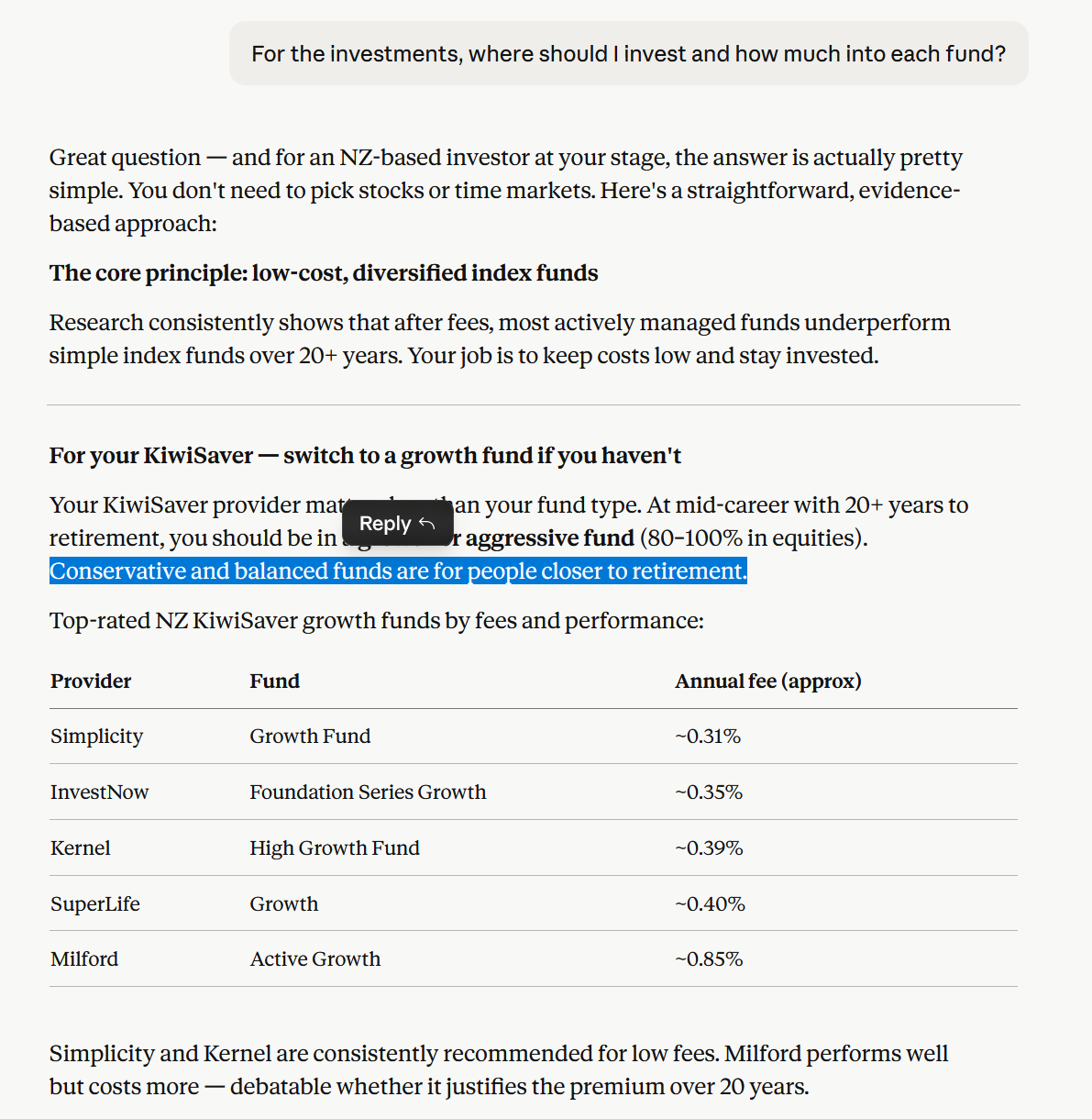

Finally I asked where to invest towards shares and how much. Claude’s response:

Again, didn’t provide specific funds per se. Just examples of some funds available.

For option A, the examples of Kernel Global 100 and Simplicity growth are very different. Simplicity growth isn’t even 100% shares. Closer to 80% shares. So not a great example.

Option B is a very high allocation towards NZ. I typically wouldn’t recommend such a high allocation. I would argue the global 100 fund is not diverse enough too.

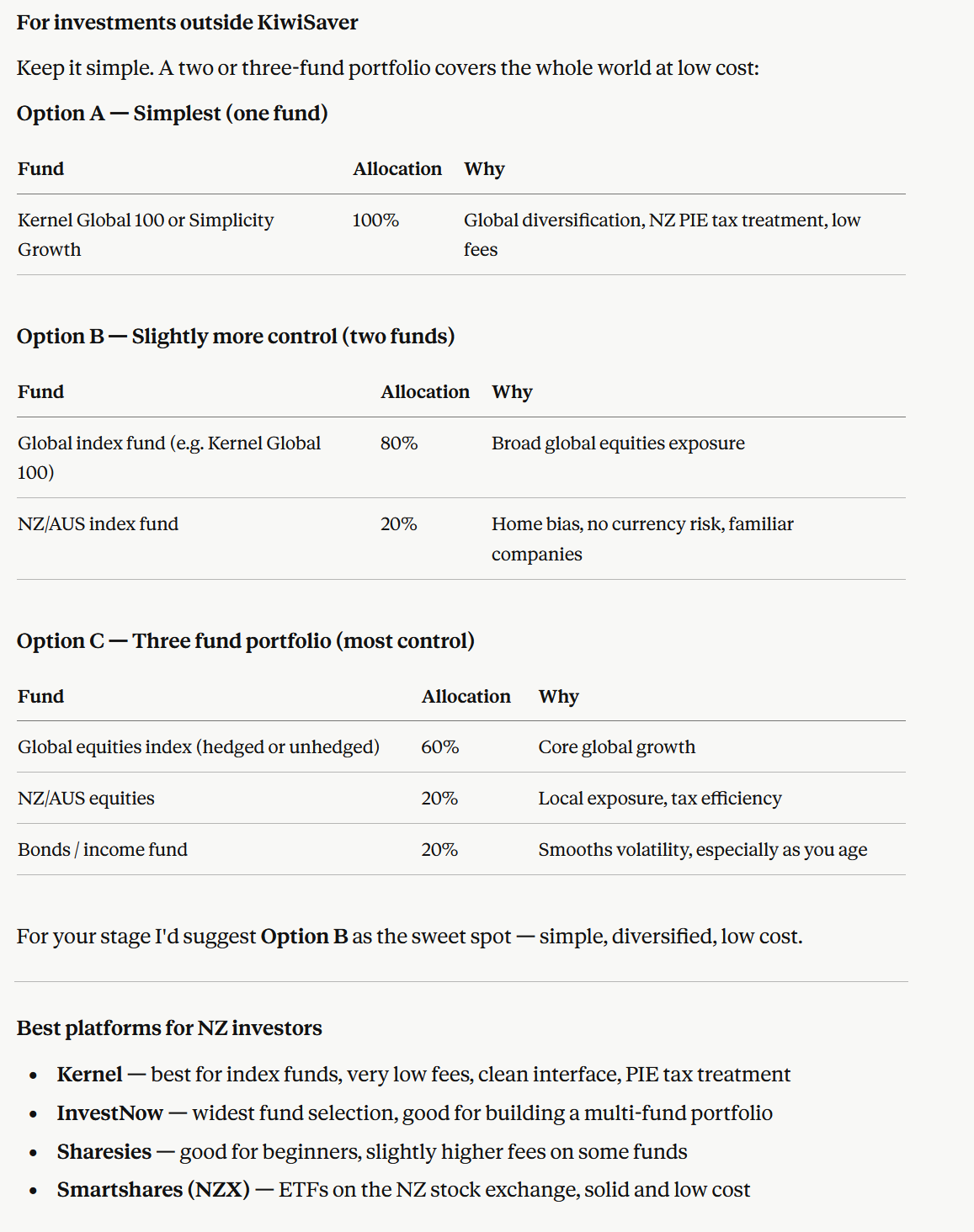

Option C is even worse. A 25% share allocation towards NZ funds (20% of 80%). Not diversified which carries risk. In addition, why have a bond allocation when you have a mortgage? To me it makes more sense to pay down the mortgage than invest in bonds.

In my opinion, some of the advice is pretty bad.

Why financial advice from AI was costly

There is too high a contribution towards KiwiSaver.

The recommended KiwiSaver fund is not aggressive enough, leaving a lot of money on the table.

The benefits of KiwiSaver are overstated.

There are no specifics around how much to invest and where unless prompted. Even if prompted there are no specific recommendations.

No specifics around how much to invest to the mortgage unless prompted.

When pushed it recommended paying down the mortgage with no knowledge of any short to medium term one off spend that may be required. Having money locked into the mortgage when it needs to be spent is bad advice.

No specifics on how much of the mortgage should be fixed and how much on revolving credit/offset. Too much general information.

There is too much overweight to NZ (shares).

Too many assumptions were made around insurance needs and how much I should be saving. Claude didn’t have any information on what assets I owned or what my annual spend was. It should be digging deeper on those things in order to offer better advice.

3 months emergency fund is not terrible advice, but it isn’t for everyone.

Putting the emergency fund against the mortgage is a valid option for a lot of people. This wasn’t even mentioned as an option.

There were not much questions asked of me from what was such a small amount of information I provided. A good adviser would ask more questions around a clients goals, spend, income, and more. I could have had plans to retire early, go part time, buy a rental property, relocate, downsize, upsize, receive an inheritance, buy a business, have kids, or any other situation, but either didn’t mention it or thought it not worth mentioning.

The implications of bad financial advice from AI

Some of this advice would result in:

Too much money towards KiwiSaver and not enough outside of KiwiSaver.

Being in the wrong KiwiSaver fund. Resulting in not enough risk and not earning as high returns as you could have. Very costly error.

Still no clearer idea on which investment funds to invest in.

Having too much of your shares allocated to New Zealand. This results in less diversification and more risk. Bigger chance of losing money than otherwise.

Still no clearer idea on how much to put on the fixed mortgage and how much on the revolving credit or offset mortgage. Or even if those are the right products for you. Choosing the wrong options again could be costly.

Unnecessarily getting more insurance than you need. Again, proving costly.

Keeping too much or too little in an emergency fund. This can impact things like your investment returns, how comfortable you are with your risk tolerance, how much insurance to have, and more.

By not recommending the emergency fund go against the mortgage, Claude’s advice doesn’t give your emergency fund money as good a return as it could otherwise.

With no deep knowledge of my situation due to not asking anywhere near enough questions, the advice of where to invest and what to do could be downright negligent and damaging.

This was a bit disappointing especially since I originally asked AI what information it needed.

Now we will take a look at someone who is much more advanced in their understanding of their financial situation.

Situation two: Financial advice from Claude for someone who is more knowledgeable and provides more up front information

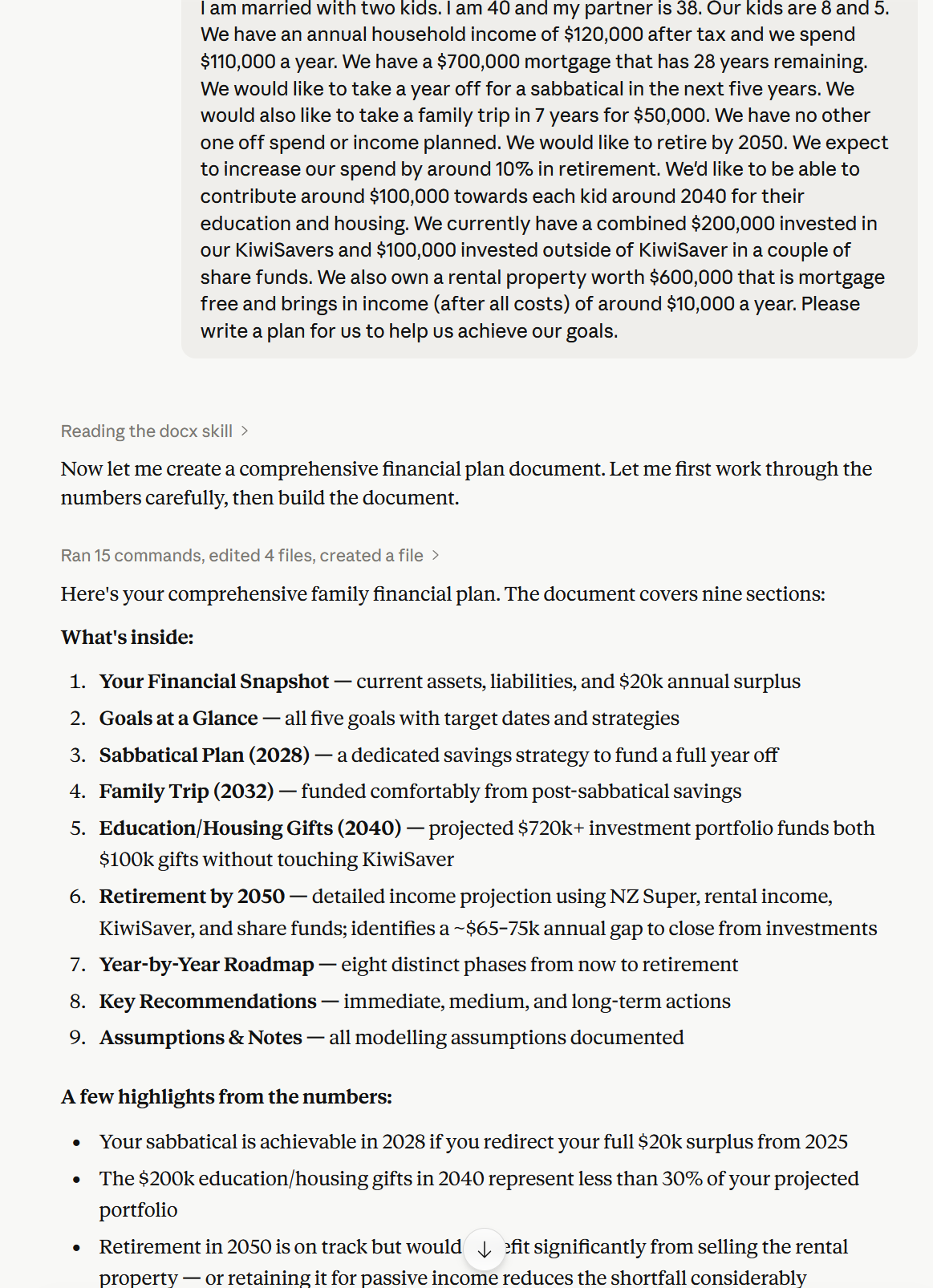

I provided a lot more hypothetical information to Claude in this example, so that it didn’t rely or need so many prompts. I gave it most of the information that it should need to offer some decent advice and here is the response:

Claude produced an attractive 10 page report which I can’t display here or the article would become too long!

mORE COSTLY ADVICE FROM cLAUDE ai

The first error is that the hypothetical net worth was calculated as $1.2 million. Claude correctly calculated the values of the assets and liabilities provided. $200,000 net worth. But what it did was assume the owner occupied house was worth $1 million. A rather big assumption. That should definitely have been queried before stating it as fact.

Claude’s plan recommends withdrawing $60,000 for a 2028 sabbatical but doesn’t make any mention that I shouldn’t be invested in shares right now. The plan doesn’t even check where my current investments are located. It could be just one company or all in NZ for all they know.

The plan recommends saving for the family sabbatical with surplus income in a savings account. No mention of an offset or revolving credit mortgage as an option which would yield better returns.

Another big omission was in the KiwiSaver calculations of Claude. They didn’t include employer, employee or government contributions in the KiwiSaver projections. These omissions result in many hundreds of thousands difference.

Claude assumes we would receive $28,000 a year income from NZ Super. Yet the current payment for a couple is closer to $44,000.

Claude assumed that our asset allocation (high growth) would remain the same all the way to age 65. However, we may need some of that money in retirement, so would need to reduce our growth allocation much sooner. Likewise, they should have mentioned reducing allocation towards growth leading up to 2040 where we planned to gift kids $200,000 in this example. Otherwise, we could lose the money just as we need it. To its credit it did reduce the KiwiSaver allocation towards growth around age 58 but it made the mistake of keeping investment return assumptions the same as if in a growth fund. Plus, some people don’t need to use their KiwiSaver money as soon as they hit retirement age, thereby reducing allocation from growth too soon would be a costly mistake.

There was no advice on mortgage structuring or where to invest. Much like the first example, specifics are lacking. I had to ask. When prompted, they suggested $5,000 of our $20,000 annual surplus to go towards KiwiSaver, $11,000 to low costs managed funds (again no mention of which funds), and $4,000 a year to mortgage pay down. When I queried why pay extra to KiwiSaver, they incorrectly stated that KiwiSaver investments are sheltered from tax. Since no specific funds or exact allocations were provided (only a general $11K a year to managed funds) I prompted for that answer. Claude came back and suggested a low cost world fund only. No NZ fund. This is not terrible advice and could do much worse. I would suggest a little NZ though for tax savings.

For KiwiSaver, Claude again recommended a growth fund. This is likely too conservative for the ages used in the example.

There was no effort made to try and understand how I felt about risk and what I may or may not be able to tolerate.

Final thoughts

As much as I point out was was missed by AI, there are some parts were OK. The recommendation to have an emergency fund, maximise KiwiSaver, and invest in a mix of shares and the mortgage is all decent GENERAL advice. But once you drill down to the specifics, there are some very costly mistakes and omissions. In some instances Claude even making certain assumptions about my hypothetical situation.

I would have thought providing Claude with more information that it would have provided better, more specific advice, and with less mistakes. However, I don’t think the advice in the second situation was any better. In fact, it was arguably worse. With more numbers, there are more assumptions and things to go wrong.

If I went ahead with some of the advice offered, it is possible I may be in an even worse position than if I hadn’t gone to AI.

For general information I give AI its credit.

For personalised and more specific recommendations I think it fails big time. And for something as important as financial planning my obviously biased conclusion is that the value of independent financial advice is not going anywhere for now. I am confident that my advice would produce significantly better results than that offered by AI today. We are talking about big money difference. As well as a greater likelihood of you meeting your life goals. I would understand you and your situation far better than AI and I would ask the questions that need to be asked. This personal touch is where AI fails.

In addition to the downright bad tailored advice and inability to ask all the right questions, there is the time commitment. It takes time to engage with AI and get the information you want. Not just the physical time, but also the mental bandwidth of worrying about a financial plan yourself and whether or not the advice you received is legit. A Financial Adviser can minimise this time significantly.

If you find the right adviser, trust is important too. You can’t trust AI, but you should be able to trust a good adviser with their advice. This is a huge factor for peace of mind.

What is really scary is how assured of themself AI sounds. There is no maybe or perhaps language in their responses. It is definitive. This is the answer. Even when that answer is blatantly unfounded.

How are we to know that the data AI collates is factual or fictitious? AI seems to take information from thousands of sources (including amateur financial advice websites such as reddit), blends them together, and spits it back out with a “trust me bro” answer. Only those who know the subject level very well may be able to pick the difference. In that case, you could argue that person (the expert) doesn’t need AI in the first place.

Because of this wide ranging sourcing of information and collating an aggregated response, that is why AI fails with specific, individualised financial advice. General information doesn’t work for specific situations. No matter how hard I tried to prompt Claude in the right direction with the required answers, it failed to deliver real actionable advice tailored to my hypothetical needs.

I think AI can be great for general information. The danger lies in thinking this general information is exactly right for you in a field as complex and with as many moving parts as your personal finances.

But AI could be great in weeding out bad information and bad actors, as well as getting more engagement from people in their finances. It’s a great starting point that wouldn’t be possible without AI.

I can easily see use cases for using AI on tasks that are easy but time consuming, or for general or common information. Things that have a small downside too, so if the response is wrong it doesn’t impact you much.

Financial advice is none of those things though. It is not general. It is highly individualised. It is not low risk. The cost of getting it wrong could be hundreds of thousands of dollars and unmet goals.

I am an expert in my field and thankfully understand when the financial advice is bad or not. If you have a decent idea of the subject matter, AI can be useful in some cases. You are more likely to be able to push back and question. You can check the output and correct any mistakes. But if you have that level of expertise anyway, you probably don’t need a Financial Adviser in the first place. In saying that, it can never hurt to get a second opinion.

However, for most of us who aren’t subject matter experts and don’t know if the information AI is providing is right or wrong, going to AI for personalised financial advice can be incredibly dangerous, costly and time consuming.

My suggestion is to leave AI for more general, common and low risk subjects. Or for subject fields that have more black and white areas of what is right and wrong. Personal finance has too much nuance and “it depends” answers to benefit much from AI.

If you need some help with developing and executing a vision and plan, then get in touch today.

The information contained on this site is the opinion of the individual author(s) based on their personal opinions, observation, research, and years of experience. The information offered by this website is general education only and is not meant to be taken as individualised financial advice, legal advice, tax advice, or any other kind of advice. You can read more of my disclaimer here.