This morning, Stuff published an article with the headline that a KiwiSaver client is $120,000 out of pocket from being in the wrong fund.

The gist is the client was in a conservative fund and is disappointed their fund provider didn’t recommend they move to a growth fund.

They only found out they were in the wrong fund when they went to a Financial Adviser for some advice. The adviser was Money Guide. A company that provides KiwiSaver advice. Money Guide pointing out that the client missed out on $120,000 from being in a conservative fund, rather than a growth fund. What a great and caring adviser right? They will be saving the client a lot of future money by making sure they are in the right fund.

Not so fast!

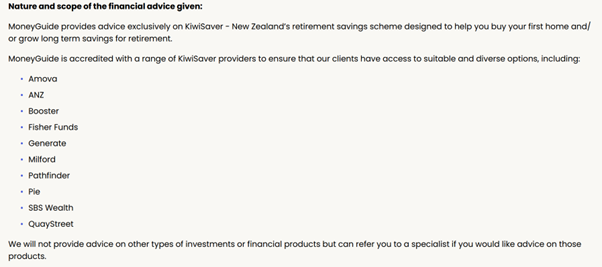

If you look at the Money Guide disclosure statement they only advise clients towards a limited range of KiwiSaver funds. Here is a couple of snippets from their disclosure statement:

Money Guide disclosure statement

Money Guide disclosure statement

Notice anything here?

All KiwiSaver products they recommend to clients are high fee active fund providers.

Money Guide staff are paid for selling these funds and the more they sell the more they pocket.

Why is this a big deal?

Well, just as important as it is to be in the right fund (conservative vs growth etc), it is just as important to be in a low fee fund.

Using the Money Guide client as an example, for them to save $120,000 over 20 years of KiwiSaver (conservative assumption), they would have needed to have earned around $2.8 million gross work income over the last 20 years.

If we assume that income trajectory continues for the next 15 years, and they go with one of Money Guide’s KiwiSaver providers paying fees of say 1.2% a year, assuming 8% investment returns, they would pay $91,350 in fees and have a year 15 KiwiSaver balance of $911,000.

Whereas, if we assume the client invests in a low fee fund of say 0.2% fees, they would pay $16,370 in fees and have a year 15 KiwiSaver balance of $1.028 million

An increase of $117,000!

Many of the providers on the Money Guide list of providers charge more than 1.2% too. Maybe the client has more than 15 years of KiwiSaver saving to go too. These changes would mean even more than a $117,000 difference in fees.

The adviser who was so concerned about the client missing out on $120,000 is adding more unnecessary cost to this poor client.

The clients high fee active fund would need to outperform the low fee fund by a whopping 1.1% (9.1%) to see the client better off.

Why advisers continue to sell high fee funds when the evidence is clear that they don’t outperform low fee alternatives is not for the benefit of the client.

Over the last 15 years, only 10% of active US large cap funds outperformed the S & P500. If you think the odds are better in Australasia it’s really not. Only 13% of Australian managers outperformed against their own index.

The data is there. Yet many advisers ignore it because it benefits them to do so. Otherwise their commission tap will run dry.

The way the Stuff article comes across as an adviser helping a client save money is not right. If the adviser was so concerned about the client saving money, they would not be recommending such high fee funds.

The information contained on this site is the opinion of the individual author(s) based on their personal opinions, observation, research, and years of experience. The information offered by this website is general education only and is not meant to be taken as individualised financial advice, legal advice, tax advice, or any other kind of advice. You can read more of my disclaimer here.